"Common advice in the past was to buy your own home so that you can avoid paying rent to the property owner. However, in this day and age, this advice may be outdated. Learn more below!" - Mitch Connolly, Senior Investment Analyst

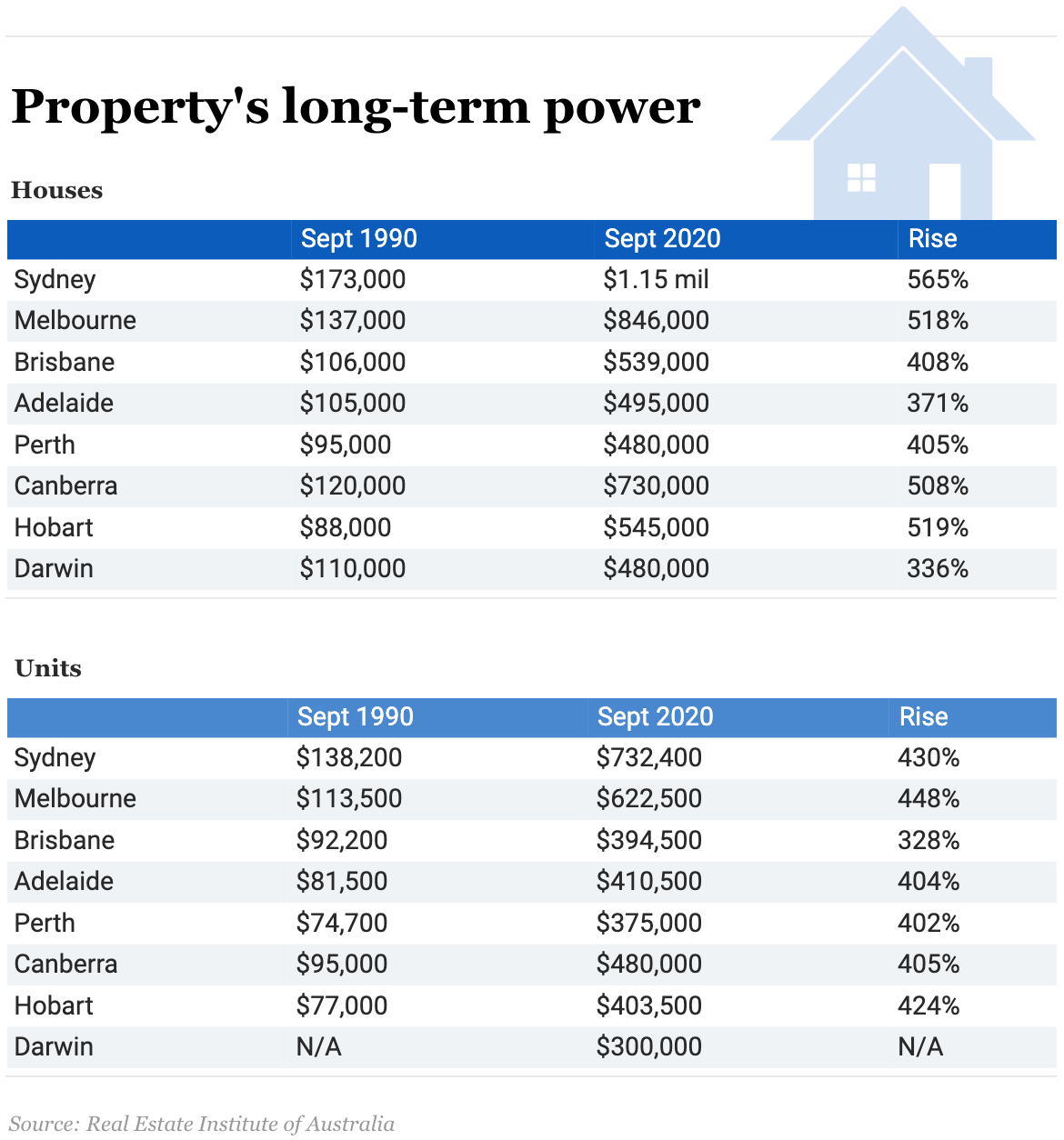

The growth in house prices in recent years has been staggering, with the average property price growth in major hubs like Sydney up over 400 per cent since the ’90s.

Today, many would-be homebuyers feel their dream home is out of reach, and more and more Aussies are looking at alternative strategies to work their way up the property ladder.

‘Rentvesting’ – buying an investment property in your budget and renting your dream home – is a strategy that has been around for years but with the post COVID property boom, this strategy is getting more attention.

Get your start in the property industry! We can help with all things property.

For Aussie Millennials the classic strategy of home ownership is drilled into us from a young age – in our parent’s generation, buying your own home was just ‘what you did’.

But, while the ability to have your own place so you can paint a feature wall your favourite shade of tangerine is appealing, many are wondering if the half-a-century old strategy of buying a home and dealing with a massive mortgage is really a smart play.

To answer that question, there’s some key things you need to know.

Paying rent is not dead money

A commonly held money belief is that when you pay rent, you’re just paying someone else’s mortgage or spending dead money. This is only half true.

Yes, your rent payments are likely to be used to pay your landlord’s mortgage. But, because the average rent is substantially lower than average mortgage and other costs on the same property, the alternative to buying yourself isn’t just renting the same place – but instead renting and having additional savings leftover.

Also, when you buy property you almost always ‘tie up’ cash savings in your property deposit. This means that if you choose not to buy the home you live in, you’ll have more cash you could use to invest.

The implication of the above is that when you think about whether to rent vs. buy, what you’re really comparing is: option 1 – renting and having higher regular savings and more cash savings to dedicate to growing your wealth through investing, vs. option 2 – using your savings and more of your regular income to buy a home.

Financial benefit of renting

For example, renting the home you want to live in could mean that you get to use your savings to buy a different investment property, potentially one of an even higher value that may grow faster because it’s a more expensive property. In this scenario you still have a roof over your head, but your investments are increasing more rapidly.

There’s a heap of moving parts here, so you need to crunch your numbers. But because property is such a large investment, putting the ideal strategy in place will likely mean a substantial difference in how quickly you get ahead with money over time.

The difference between renting and buying

In Australia under the current tax laws, paying mortgage interest and property costs like strata isn’t tax deductible on your own home, but it is on investment properties. This means that if you were to consider buying the same property as your own home vs. buying it as an investment, the after tax cost will be different.

Whether the different after tax cost of your property purchase is positive or negative depends on a number of factors like your taxable income, marginal tax rate, current interest rates, your mortgage and other ongoing property costs. But you should be aware that there is always a difference.

Your home isn’t really an investment

Another commonly held belief surrounds that having a highly valuable home is good because it means you’ve got a big asset behind you. But while it’s technically true that your home is a financial asset, if you intend to live in your home forever it’s not really an asset that will give you any real financial benefit.

This means the higher the value of your home, the more of your wealth is effectively ‘trapped’ in an asset that doesn’t contribute to your true wealth.

I’ve found that finding the right balance between your overall wealth and the amount of your wealth tied up in your home is one of the biggest factors that drives true wealth. If you get the balance wrong, and you end up like the nobles in the UK that live in castles they can’t afford to maintain, with no money to allow them to live a good lifestyle.

An extreme example clearly, but one worth keeping in mind given house prices around Aussie CBD areas.

Stepping stones to your dream home

Be aware that if you do make the decision to rent today, it doesn’t need to be a lifelong choice. If the numbers make sense and you’re comfortable renting for a while, you can use your extra savings to build assets and make it easier for you to buy your dream home in the future.

For example, if your ultimate goal of buying a $1.5m property is out of reach today, if you were to buy an investment property for $750k, you’re now halfway toward the total value of your dream home. Then, through buying another $750k investment property in a few years you should be close to the ability to sell both properties and afford the home you really want.

Be aware there are other factors to consider like taxes and costs of buying and selling property, but as a ballpark approach I’ve seen this work well for a number of people in the past.

The alternative strategy of not getting into the property market while house prices continue to rise has proved much less effective historically.

How to figure out what’s best for you

There are a lot of factors to consider for you to accurately answer whether renting is better than buying property, don’t buy into the popular beliefs that there’s one approach that works for everyone. The right answer really depends on you.

It depends on where you’re at today financially, what sort of property you’re thinking about buying, and how your situation will change over time. A property purchase is a long-term investment, so don’t fall into the trap of short term thinking here.

Buying a property is an emotional purchase, and your feelings are important. But they’re not the only important thing. I’ve seen too many people make property decisions based only on how it ‘feels’ for them without looking deep enough into the numbers, only to regret it later.

The key to making the best property buying choices for you is to consider your emotions alongside the numbers. You should map out your current position with assets and debt alongside your income and expenses, and then think ahead as to how these will change over time.

Think about any bigger changes like starting a family, starting a business, childcare and schooling costs, extended travel, etc. I call this your ‘lifestyle baseline’. Once you have this baseline in place, you’re ready to start overlaying your property purchase, looking at the difference between rentvesting vs. buying as an owner occupier.

Check out your numbers and look at the impact on your day-to-day over the next few years, as well as your bottom line asset position 10 to 20 years from now. There will be a financial difference between the two scenarios, but as mentioned above there’s also an emotional difference.

You need to think through what’s most important to you, and again look to find balance.

Get your balance right and you’ll end up with a property that gives you the financial outcomes important to you and the personal or lifestyle benefits you want. This approach also allows you to identify and manage risk, and ensure your property purchase fits with the lifestyle you want to live today and into the future.

This can be difficult to do on your own, so don’t be afraid to get good help here – it will pay for itself many times over.

The wrap

Buying property is a massive decision that will impact your financial situation for years, if not decades to come. The emotions and peace of mind attached to renting vs. buying property are also a big deal. Balance is key here.

There are a lot of myths, misconceptions and stigma out there around buying property – don’t buy into the hype. Take the time to map out the ideal strategy for you and you’ll benefit today and for years to come.

Access leading property and finance professionals! Book an obligation-free call today.

Source: News.com.au

Nash, B. (2021, April 13). Clever way to beat housing boom. NewsComAu. https://www.news.com.au/finance/money/investing/renting-buying-or-rentvesting-which-is-better-financially/news-story/ae1518898ba4ba80b259c132f34a5805