Posted on: 8 Oct 2015

ASX loses $55 billion in savage resources stocks sell-off

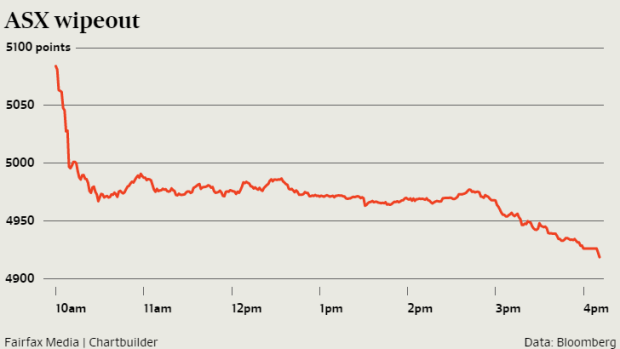

ASX200 index plummeted 3.8 per cent to 4918.4, shaving off nearly $55 billion in market cap, while the broader All Ordinaries fell 3.6 per cent to 4958.1.

A shock decline in UK-listed mining giant Glencore coupled with a sharp drop on Wall Street triggered panic selling in resources stocks, sending the local market to its lowest level in more than two years on Tuesday.

Energy and mining stocks - including a staggering 6.6 per cent drop in BHP - led the falls, as the benchmark ASX200 index plummeted 3.8 per cent to 4918.4, shaving off nearly $55 billion in market cap, while the broader All Ordinaries fell 3.6 per cent to 4958.1.

It was the worst day on the market since August 24, when the ASX200 closed 4.1 per cent lower, and the lowest for the ASX200 since July 2013.

Miners were belted after shares in the UK-listed mining and trading company Glencore fell almost 30 per cent after analysts suggested the stock could be nearly worthless. Glencore shares, which closed at a record low, have been under pressure over concerns it is not doing enough to cut its debt to withstand a prolonged fall in global metals prices.

Hefty falls on Wall Street, driven by concerns about China's economy and the timing of the Federal Reserve's next interest rate move, further hurt local sentiment.

"It's not just commodities, it's across the board...the banks are down as well," said Morgans senior dealer Luke McElwaine. "You know it's a big day when BHP is down 6 per cent. It's not often you see numbers like that from these big stocks.

"It's a combination of Glencore's rout, Wall Street being down and making up for the fact that we were up on Monday.

"I'm not sure we've learnt anything new that's justified a big sell-off like this but it's just that sentiment is so bad."

The benchmark index is now down nearly 9 per cent in the September quarter, on track for its worst quarterly performance since 2011. For the month, it is down 4.4 per cent, after slipping 8.6 per cent in August - its poorest monthly show since the global financial crisis.

"We wouldn't be surprised to see the (index) print 4700 before it finds any real support, now that 5000 has given way," said Chris Conway, head of research, Australian Stock Report. "The worry is that the rout is not yet done."

"There is nowhere to hide ... with every sector under intense pressure," said Mr Conway.

"The miners are bearing the full force of investors' ire. However, amid worries about global growth emanating out of China, the massive slump in Glencore overnight and news filtering through that hedge funds around the globe are dumping commodities risk."

The big miners were walloped, with BHP crashing 6.6 per cent to a seven-year low $21.61 and Rio Tinto tumbling 4.6 per cent to $46.52.

The big four banks were also punished, with ANZ losing 3.7 per cent to $26.38, Commonwealth Bank falling 3.5 per cent to $70.51, National Australia Bank down 3.6 per cent to $29.20 and Westpac declining 3.8 per cent to $29.10. Fellow blue-chip Telstra also fell heavily, down 4.3 per cent to $5.49.

Among other mining stocks, Fortescue fell 6.4 per cent to $1.67, and Arrium dived 5.5 per cent to 8.6 cents.

On a percentage basis, energy stocks were the day's worst performers, with Paladin down 13.1 per cent to 16.5 cents, Karoon Gas 11.1 per cent to $1.67, Origin Energy 10.4 per cent to $6.10, AWE 9.2 per cent to 64 cents and Santos 9.1 per cent to $4.28.

In other economic news, last week's jump in consumer confidence following Malcolm Turnbull's ascension to the nation's top job proved to be short lived.

The ANZ/Roy Morgan weekly consumer confidence index fell 3.4 per cent last week, after jumping 8.7 per cent the previous week in reaction to Turnbull winning the Liberal leadership and becoming Prime Minister.